Shocking? Yes. Exciting? Possibly. Discouraging? Maybe. Long term? Likely not.

This month’s home sales data that was prepared by Kyle Snyder with First American Title shows some interesting things in our market.

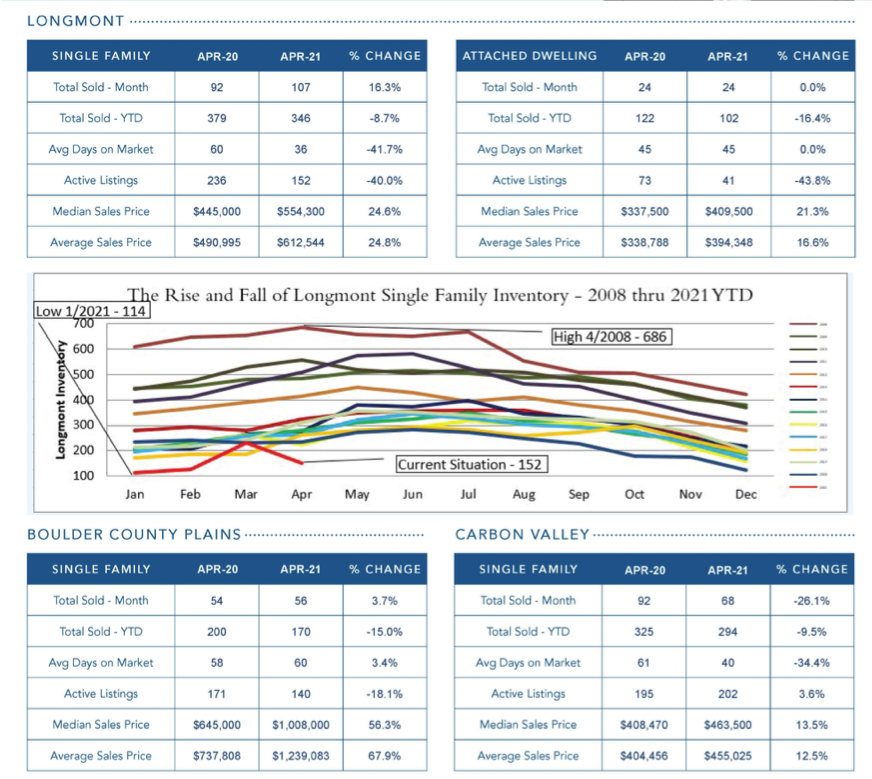

First off, “Shocking?” This is the first time that our average home sale price has exceeded $600k! Great news if you are selling your home, or invested in Longmont’s future many years ago. I’ve been born and raised here, it’s shocking to see. Also, our active listings are down 40% over April of 2020. Now, let’s get real for a moment: last April we were all doing something new…staying inside, not going out, and for many people...not selling their homes as pictured here. Active listings were down almost 25% then as well. If you are a buyer in this market, you are likely shocked at the patience you need, and the focus you and your agent need with almost 65% fewer homes available from two years ago.

“Exciting?” Well, I said possibly. If you are a seller right now, you are likely excited unless you are selling only to buy again in town…in a popular price range. Right now, our popular price range is $400k-$1.5m….so likely anything. So, for buyers…if you like adventure…sure…. it’s also exciting. Sellers are getting more for their homes than they have in years…and in some cases ever. And, unlike 2008…the money is arguably more legitimate. Boulder County is blessed with strong industries, an affluent workforce, and a number of desirable recreation attractions. So the loans that are being made on these homes, are theoretically safer bets for the mortgage market and therefore the real estate market simply because they are not just fogged, mirror borrowers. We are seeing many people putting down 10’s of thousands and in some cases, hundreds of thousands making the LTV’s a little easier to stomach with these higher prices.

“Discouraging?” Here I said maybe. These price increases are huge. Kyle said in his report that: In last month’s report, the price increases for the average and median sales prices in the Boulder County Plains were 43.1% and 64.4% respectively. Those are HUUUUUUGE jumps. This month… they were even HUUUUUUGE-er at 56.3% and 67.9%. This can’t be good. If this keeps up, Longmont prices could look like Boulder in less than 2 years. For anyone that has lived here for more than a few years, you know that when someone says “our prices may be near Boulders in a couple of years” you don’t just shrug this off and say oh well. For a seller that needs to sell now…that can be great news or tricky news….when is the right time to capitalize to the fullest extent on your investment? For buyers, its earth-shattering…many will just keep moving out east as the typical comment of “Front range home values start at the Flatirons and just slide east….keep going until you find what you can afford”. However, to contradict this thought of discouragement….how many of you have said “I wish I would have bought in Boulder before it really became “Boulder”? Well, don’t look a gift horse in the mouth. Some of these stats might be encouraging to some looking to speculate. One thing is true…our population as a country and specifically a state are growing every day, and I’ve yet to find many people that feel like a roof over their head is not on their list of important needs.

“Long Term?” I personally don’t think so. But, believe me…I don’t have a crystal ball. While it’s not an end-all say-all to the inventory issue, one thing that I noticed over this last year of reduced inventory is that during the pandemic we were showing many vacant homes. For me, it was literally 9 out of 10 homes had no one in them. In talking to my sphere of influence and friends many people were simply not comfortable with people going in and out of their homes during the peak of the pandemic. It was only around September of 2020 when I started to notice that I was walking into homes that had an occupant. Slowly and slowly it seems to be more frequent that we get calls from people ready to sell, and will still be in the home. Oddly, several of them are not relocating to Longmont or the area which is the best thing for this market. Inventory that is not being traded with other inventory…so a “True Addition” to the inventory shortage. I don’t think that the pent-up pandemic inventory is going to change the entire market, but my hope is that it will help even things out a bit…and lessen the curve to a more sustainable increase in price. If we pair some more inventory with buyers having to head out east and out of Longmont…the two combined might result in a little shift in the craziness. I still remember the days of a balanced market….homes on the market for 25-35 days, getting fair offers, buyers having the opportunity to look at 5-10 homes and then decide. Everybody won.