“I am going to wait until prices drop during the pandemic”

Commentary by Kyle Snyder – First American Title.

Local real estate sales in August 2020 just blew my mind! We are clear on what is happening around us economically due to the lockdown restrictions. Retailers, restaurants, and businesses, big and small are struggling. People are out of work and many have died, so why is real estate doing so darn well? There must be an overwhelming belief that the future will bring good fortune, so people are willing to take a leap of faith that the economy won’t sink. The world is looking forward to the time when lockdowns end, the pandemic wanes, the election is over, and kids go back to school. Buying real estate is a huge commitment of one’s personal fortune, no matter how big or small the home; and right now, people are making that commitment much more than expected.

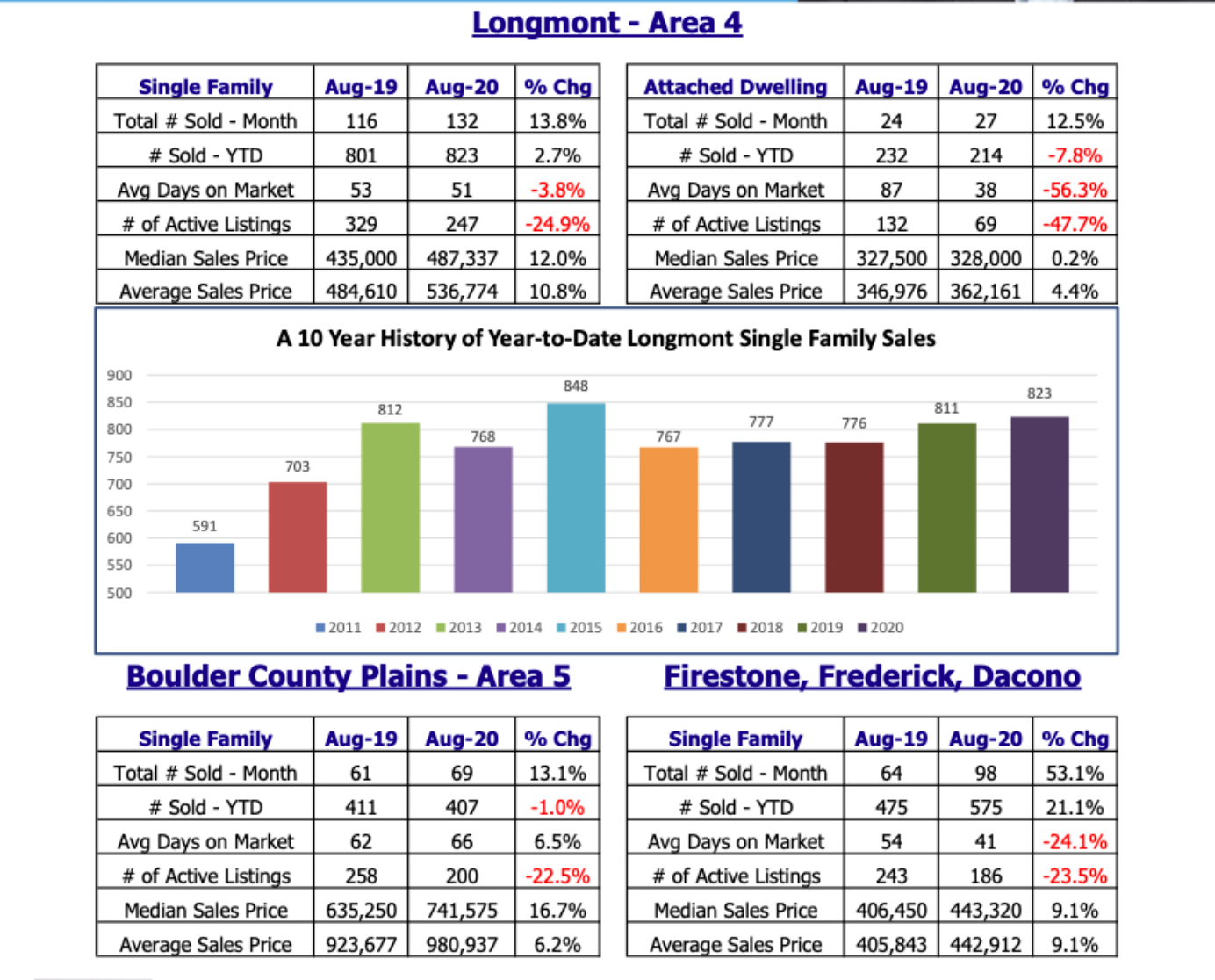

The end of August is the end of the 1st two-thirds of the year. Given all that’s happened in the world this year, I thought I’d look at the total sales in the 1st two-thirds of each of the past 10 years. How did a global pandemic and lockdowns affect the real estate market? Look at this month’s chart. So far in 2020 we closed the 2nd most single-family homes in the past 10 years! 2nd MOST! And the 3rd most for an August over the same 10-year span. So, from my perspective, there has been nearly zero long-term impact on the local real estate market from covid despite the below-average sales totals in April and May.

To tell a story in stats, one should look at the big picture, as well as the more focused little picture. If they tell the same story, you should have a clear picture, so let me clear things up, the big picture includes the record-breaking sales mentioned above. Consider this as well: all four markets covered by this report experienced higher year-over-year monthly sales in August, along with fewer listings, higher median and average prices, and steady to lower average days on market. Those results are clearly in the right direction.

In August, Longmont set its all-time high average sales price for a single-family home. In fact, the average of $536,774 is $32,000 higher than the previous high, set in March of this year. This monthly average has eclipsed $500,000 on a handful of occasions, but this one takes the cake. If sales hold steady for the remainder of the year, and it looks like they will, we could end up with a yearly average price of over $500k for the first time ever. Right now, it sits at about $501k. (In case you were wondering, Boulder’s average for the year sits at $1,233,783). The strength and resiliency of our local market is obvious by now. It’s the “how is this happening with so few listings?” that’s the real head-scratcher for me. Maybe I should quit being amazed…

Attached homes in Longmont are still doing well despite a mild shift away from the product in general. Apparently, people don’t really love to live in close quarters to their neighbors during a pandemic. I understand this, but I don’t see it being a massive driver of the single-family market increases. There isn’t a glut of attached listings; days on market dropped significantly compared to last year; and prices increased slightly; all indicating they are still performing well in this area.

There is an emerging theory about buyers who are fleeing condos and big cities. It says they are looking for more room and possibly two home offices since so many couples have figured out how to work from home. It seems like this might be having some influence on our local markets. The Boulder County Plains are just as hot as anywhere else… and they are about twice as expensive as anywhere else. Sales and prices are up, and inventory is down. This phenomenon is clearly regional in nature and not just specific to Longmont.